Taxpayers can utilize IRS Form 709 to report chargeable gifts made throughout their lives and apportion the lifetime use of their decade's transfer tax exemption. When a person dies, leaving their possessions to their heirs, the value of their estate is taxed. Because of the federal gift tax, generous donors could avoid paying estate taxes by distributing their wealth to others tax-free while they are still alive. Because there is no property to convey after death, if gifts are not reported on Form 70, they will not be shut off from the IRS and will be subject to any tax that may be payable.

Is Form 709 Used By Anyone Else?

The donor, not the recipient, is responsible for any taxes due on a gift. In addition, if the donations are not exempt, the gift sender is responsible for executing and submitting Form 709 to the IRS. In most cases, a gift tax is levied on the transfer of ownership of one individual to another if the receiver does not pay the market price in return for the property. The gift tax would indeed be due on the differential between the home's fair value and what the parent paid if they gave their child their house for $1. You'd need to fill out IRS Form 709 for that.

Where Can I Find a Form 709?

You are using the IRS's interactive Form, which can do 709 directly from the IRS's website. You can fill it out online, save it, and print it.

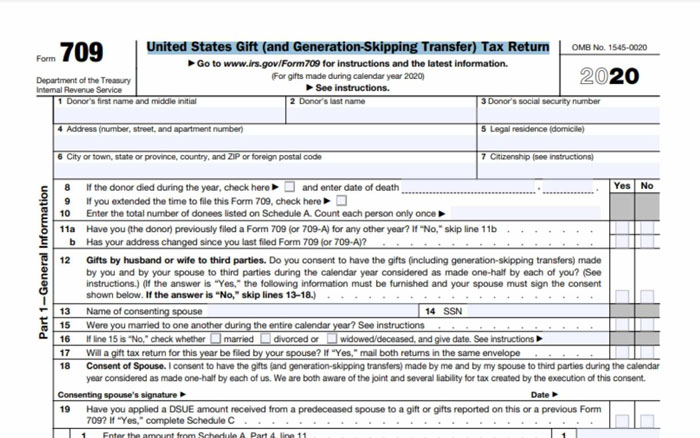

Form 709: How to Fill It Out and Read It

Every time you give more than $15,000 to a single person in a calendar year, you must file Form 709. The annual Exclusion for the tax year 2021 is $15,000, and it will rise to $16,000 in the following year. The first section of Form 709 asks you to identify yourself and the source of your present or gifts and then fill in the blanks. After that, you'll learn how to figure out how much tax you owe in Part II. To avoid gift tax, you can use Schedules It through a D to take advantage of specific tax advantages.

The Exclusion Is an Annual Event

In the phrase "annual exclusion," the word "annual" makes a big difference. On Nov 31, 2020, you could have given your daughter $15,000; on Jan 1, 2021, you may have offered your child another $15,000, for a maximum of $30,000, without triggering a gift tax. Let's take another look at this. Who will owe taxes on $30,000 if you raise your kid by $15,000 to buy a vehicle and another $15,000 to clear off their credit debt in much the same tax year—minus the $15,000 exclusion for that year.

Despite being indexed for inflation in 1997, the yearly Exclusion can only be raised by $1,000 every year, so it cannot increase by more than $1,000 or less than $1,000. In 2009, 2010, 2011, and 2012, the exclusion was $13,000; in 2017, 2019, 2021, and 2022, it was $15,000 per year. In 2022, it will rise to $16,000.

Sharing Your Gifts Amongst Your Friends and Family

The annual Exclusion for married couples might be doubled by "splitting" their presents between them. To buy a car, your spouse might offer your child $20,000 and another $20,000 to pay off credit card debt, which totals $25,000 total. Their options are to declare $5,000 in deductible gifts on Form 709, or they can submit Form 709 and disclose that perhaps the two of you have decided to split up the facilities following the $15,000 annual exception.

If you did so, you might be counted as making a $10,000 contribution under the $15,000 yearly exclusion. Even if all $20,000 came from an institution in your couple's sole name, which would owe no tax.

The Unified Credit For All Time

Gifts are excluded from gift tax under the Income Tax Act for the donor's lifetime. A $30,000 present to your child could be taxed at a rate of 15%, or it could be charged to your lifetime gift exemption if you use this example as a guideline again. You won't have to pay gift tax on transfers of up to $11.7 million made in a lifetime in 2021, but there is still a catch.

The term "unified credit" refers to the gift tax and the death tax. Both have the same exemption. The lifetime unified credit is reduced by $500,000 if you give your child gifts above and beyond the annual exclusion thresholds. You'll have $11.2 million in your estate when you die to protect from taxation.

E-Filing of Form 709 Is Possible

Who must send form 709 to the IRS in the traditional manner? The IRS only accepts printouts of this tax return, which must be mailed in USPS-stamped envelopes. Electronically filing the Form is impossible.