Are you drowning in debt? You're not alone. With skyrocketing living costs and stagnant wage growth, many people carry high debt levels and need help to get out.

Too much debt can cause immense anxiety that affects every part of your life. But what's the best way to tackle this problem? Understanding your Debt to Income Ratio (or DTI) is the answer.

In this blog post, we'll provide step-by-step actionable tips and advice on how to lower your DTI and decrease other kinds of outstanding debts efficiently while maintaining a healthy lifestyle and saving money for future goals. Read on to find out more!

What Is Debt-to-Income Ratio

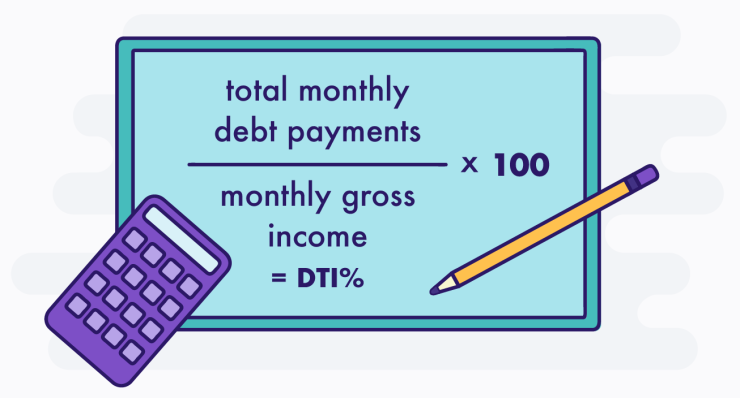

Your Debt-to-Income Ratio (DTI) calculates your total monthly debt payments to your gross monthly income. It helps lenders and creditors assess how much of your income goes towards existing debts and how much you have left for other expenses. The lower the ratio, the better your chances of being approved for credit or a loan.

Two types of Debt-to-Income Ratios are:

1. Front-end Ratio

This measures your housing expenses, which include mortgage payments, homeowners insurance, and property taxes. It should be at most 28% of your gross monthly income.

2. Back-end Ratio

This DTI calculates all your debt obligations like credit cards, student loans, and car loans as a percentage of your income before taxes. It should be at most 36%.

If your DTI is higher than these two thresholds, it is time to start taking steps to lower it.

How Is Debt-To-Income Ratio Calculated

To calculate your Debt-to-Income Ratio, you must first add up all your monthly debt payments. These include the following:

• Mortgage/Rent payments

• Credit card payments

• Car loans or leases

• Childcare expenses

• Student loan and other educational payment plans

• Personal loans and other lines of credit

• Any other regular monthly payments related to debt

Once you have added all your debt payments, you can divide the total by your gross monthly income. This calculation will give you your DTI ratio. To ensure accuracy, include any extra income you receive consistently, such as alimony or child support, disability benefits, or rental income.

How to Lower Your Debt-to-Income Ratio

Now that you understand your DTI ratio and its calculation, you can take the necessary steps to lower it. Here are a few ways to do this:

Avoid taking on more debt.

When lowering your DTI, the first step is to avoid taking on more debt. Many use credit cards and loans as a "quick fix" for short-term cash flow issues. However, this can lead to an even higher overall debt due to high-interest rates and fees.

If you need emergency funds, exhaust all other financing forms, such as personal savings or family members, before turning to banks or lenders. Additionally, reducing existing debts is important instead of adding new ones.

Make a plan for paying off your credit cards.

Paying off your credit cards is crucial to lowering your DTI ratio. List all your outstanding credit card debt, including interest rates and monthly payment amounts.

Then, prioritize which debt to pay off first based on interest rate - it makes sense to tackle the ones with higher interest rates first, as this will help you save money in the long run.

Once you know which debts you'll focus on, you can make a budget to ensure you are allocating sufficient funds toward paying off your debt each month.

It would help to establish a timeline for how quickly you want to pay off each credit card. Creating and sticking to a plan can lower your DTI ratio and eventually be debt-free.

Consolidate Debt

One of the most effective strategies to reduce your Debt to Income Ratio (DTI) is to consolidate debt. By consolidating different debts into one, it can help make repayment easier and reduce interest rates and fees associated with multiple accounts, allowing you to save money in the long run.

Consolidation can be done through a loan or a balance transfer card, with advantages and disadvantages that must be weighed before taking action.

Lower Your Interest on Debt

Lowering your interest on debt can be a great way to reduce your Debt to Income Ratio (DTI). By negotiating with creditors or exploring different loan options, you can lower the interest you pay for your debts.

To do this, gather all relevant information about your finances and debts. Then, make a plan to help you prioritize payments and create an achievable timeline for reaching your debt goals.

When considering loan options, consider the APR and fees associated with each option before deciding. Lastly, ensure you understand all terms and conditions attached to the loan before signing any paperwork.

Increase Your Income

The best way to reduce your Debt to Income Ratio is to increase your income. This practice can be done through side hustles, finding a better-paying job, or asking for a raise. There are online resources that can help you find additional sources of income as well.

Many employers also offer health and retirement benefits packages that can help add to your income. Consider negotiating with creditors for lower monthly payments or consolidating multiple debts into one loan with a lower interest rate.

Working hard and making smart financial decisions will help you pay off debt faster and reduce your DTI in the long run.

Do pay off existing debt

Before you attempt to lower your Debt to Income Ratio (DTI), ensure all existing debts are paid off first. It's important to prioritize paying off the highest interest rate debt first, as this will save you the most money in the long run.

Moreover, paying off each debt will help improve your credit score and give you more options for future loans or refinancing. To accelerate the payment process, make frequent payments, such as weekly or bi-weekly, instead of monthly.

Increase the amount you pay monthly toward your debts.

The best way to lower your Debt to Income Ratio (DTI) is by increasing the amount you pay monthly toward your debts. This practice could include making additional payments, reducing loan interest rates, or consolidating debt into one loan with a lower interest rate.

Budgeting for these extra monthly payments is important so that you're not over-extending yourself financially and can continue living a healthy lifestyle while paying down your debt.

Additionally, some lenders may offer rewards programs to help you save money if you make regular payments on time or remain within a certain balance range. By taking advantage of these programs, you'll be able to reduce your DTI faster while still enjoying all the benefits of being creditworthy.

FAQs

What if my debt-to-income ratio is too high?

If your debt-to-income ratio is too high, it can significantly reduce your ability to make large purchases such as a home or car.

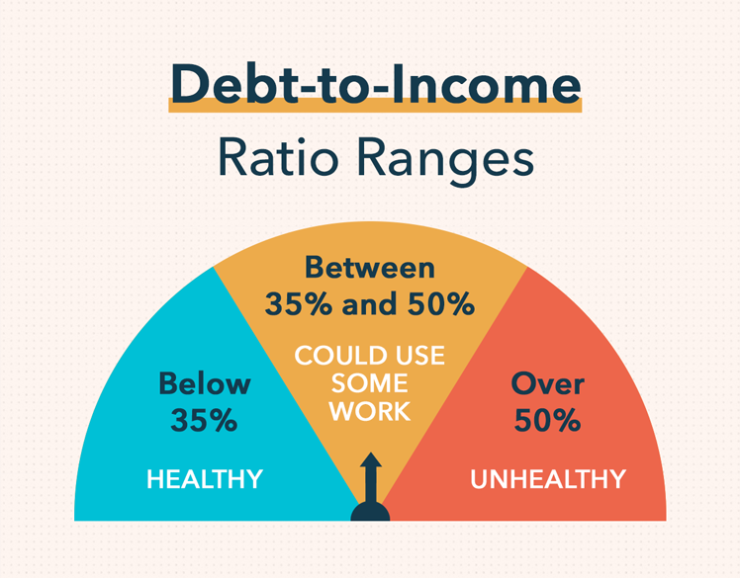

What is a healthy debt-to-income ratio?

A healthy debt-to-income ratio is typically considered to be anything below 36%. Anything above 38% should be considered an area of financial concern.

What goes against the debt-to-income ratio?

Debts considered when calculating your debt-to-income ratio include credit card debt, auto loans, student loans, and any other installment loan.

Conclusion

Understanding your debt-to-income ratio is the first step to reducing and managing your debt. Lowering your debt-to-income ratio can be done through various methods, such as creating a repayment plan for credit cards, consolidating debt to lower interest rates, increasing income, and paying off additional debts each month or as soon as possible. It may be difficult to make these changes, but making them will increase the chance that lenders will look favorably upon you if you decide to apply for loans or lines of credit.