Buying a home is an exciting milestone, but understanding the details and financial implications of such a big purchase can be overwhelming.

Before you start the home-buying process, it's important to get familiar with the factors lenders consider when deciding on mortgage loan approval—one being your credit score.

What exactly is considered a good credit score for a home loan? Read on to learn more about what kind of credit score you need for pre-approval mortgages and advice on improving yours if needed.

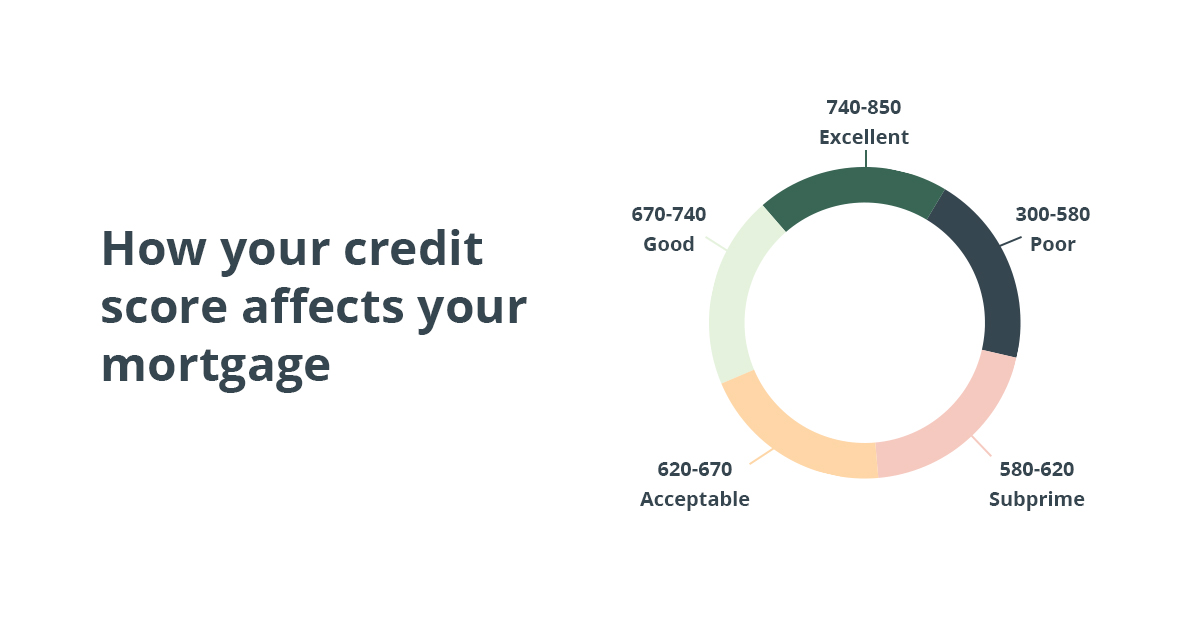

How Your Credit Score Affects Mortgage Rates

Your credit score is an important part of the home loan application process, as it can directly influence mortgage rates. Generally speaking, a higher credit score means you'll be offered a better interest rate on your mortgage loan.

That being said, most lenders require a minimum FICO score of 620 to qualify for pre-approval home loans; while some may still approve lower scores, they often come with higher interest rates and other associated costs.

Improving your credit score should be one of your top priorities if you're looking for a good home loan deal.

What Credit Score Is Needed to Get a Mortgage

When applying for a mortgage, lenders generally require borrowers to have a minimum credit score. The higher the credit score, the better your chance of receiving pre-approval and favorable loan terms.

Conventional Loans Minimum Credit Score: 620

Most lenders require a minimum FICO Score of 620 or higher for approval for conventional loans. However, certain lenders may allow lower scores with additional scrutiny or other compensating factors.

Additionally, if you're putting down less than 20% of the home purchase price as a down payment on your loan, you may be subject to stricter credit requirements and PMI (private mortgage insurance).

Jumbo Loans Minimum Credit Score: 700

Jumbo loans are often more expensive and require higher credit scores than conventional mortgages. The minimum credit score required is typically 700, although some lenders may allow for a lower score with additional considerations.

FHA Loans Minimum Credit Score: 500

The Federal Housing Administration (FHA) requires a minimum FICO® Score of 500 for approval. However, it's important to note that the FHA also stipulates that borrowers with credit scores between 500-579 will need at least a 10% down payment to secure an FHA loan.

USDA Loans Minimum Credit Score: 580

For USDA loans, lenders typically require a minimum credit score of 580 or higher; however, there are instances where lenders may increase the credit score requirement to 600.

VA Loans Minimum Credit Score: 620

Regarding VA loans, most lenders require a minimum FICO Score of 620 or higher to secure the loan. While some lenders may allow for lower scores, they may require additional compensating factors such as a higher debt-to-income ratio.

Knowing what kind of credit score is needed for pre-approval can help you plan and improve your credit before beginning the home-buying process. If your current score falls below these requirements, start by reviewing your credit report and disputing any errors, then work on paying down any lingering debts to raise your score over time.

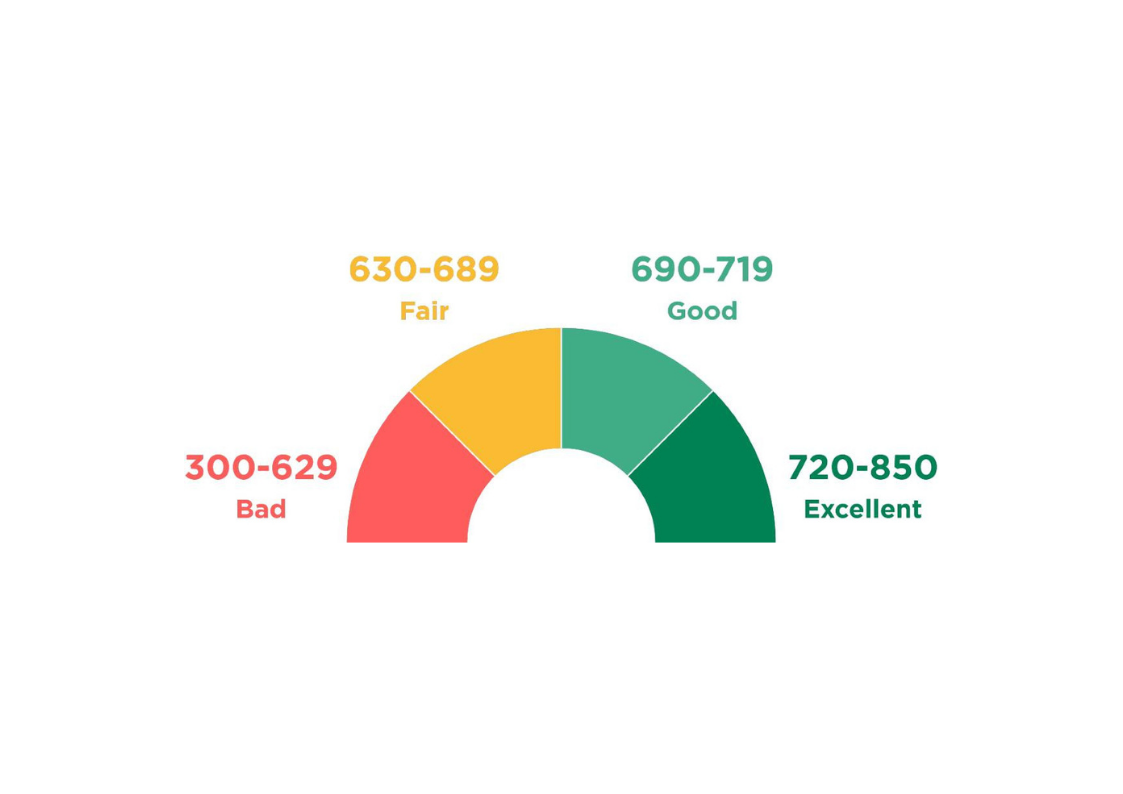

Can You Get a Mortgage With a Bad Credit Score

A good credit score is essential when applying for a mortgage loan. Generally, the higher your credit score is, the better interest rate and loan terms you'll be eligible for. Lenders typically consider scores over 700 "good" or "excellent."

Qualifying for a home loan with a lower score may still be possible, but expect less favorable terms and more stringent requirements. Depending on your lender, you may need a minimum of 500-580 to qualify for an FHA loan or 620-640 for a conventional loan.

However, many major lenders require a 680 or higher to approve you for pre-approval.

How to Prepare Your Credit for a Mortgage

Pay Your Bills On Time

This may seem obvious, but paying bills on time is one of the most important factors lenders use when evaluating an applicant's creditworthiness. Ensure all debt payments are current before applying for a mortgage loan so there are no issues during the loan review process.

Check Your Credit Report For Errors

It's important to check your credit report for errors or mistakes before applying for a mortgage loan. If you find any, dispute them with the credit bureaus immediately to correct them before being assessed by lenders.

Keep Credit Card Balances Low

Having high balances on your credit cards can send red flags to lenders that you are overextended and unable to manage your finances well, which could hurt your chances of getting approved for a mortgage loan. Try to keep credit card balances at 30% or less of their available limit to look more favorable in the eyes of lenders.

Don't Open New Lines of Credit

Before applying for a mortgage loan, it's wise to avoid taking on any new lines of credit that could lower your score and negatively impact your chances of being approved.

Pay Off Smaller Debts First

Although paying off smaller debts won't significantly improve your overall credit score, it can help you better manage cash flow and ensure all bills are paid on time before the loan is considered.

Consider Refinancing Any Long-Term Debts

If you have any long-term debts, such as a car or student loans, consider refinancing them into more favorable loan terms with a lower interest rate. This tip will help free up more cash flow and lower your monthly payments, making you look more attractive to lenders when applying for a mortgage loan.

These simple tips can best prepare your credit for a mortgage and improve your approval chances. Remember, having good credit is essential if you want to get pre-approved for a mortgage loan - so take the time to check your score and address any discrepancies before applying.

FAQs

What is a good enough credit score to buy a house?

Generally, most lenders look for a credit score of 620 or higher for home loan approval. However, this number can vary depending on the type of loan you're applying for and other factors, such as your debt-to-income ratio (DTI).

Can I get a home loan with a 580 credit score?

If your credit score falls below 620, you may still be able to qualify for a home loan with the help of a cosigner or other special circumstances. FHA loans are an option for borrowers with scores as low as 580. Before applying, it's smart to speak to a mortgage specialist and review your options before making any decisions.

How much of a loan can I get with a 650 credit score?

The amount of loan you can qualify for depends on your income and DTI ratio, but having a credit score of 650 or higher puts you in a good position to get approved for a home loan. Again, talking to an experienced mortgage lender is the best way to determine how much of a loan you may be eligible for.

Conclusion

When getting a mortgage, having a good credit score is crucial. A high credit score shows lenders that you are responsible and can reliably meet your financial obligations. Your credit score is one of the most important factors in determining your eligibility for a loan and the interest rate you may be charged. Improving your credit score is always possible; you can increase it and become eligible for competitive rates. If you're wondering what credit score is needed for a home loan, the answer can vary by lender but typically requires at least a 620-640 range.